ViDA in a nutshell and key e-invoicing updates in Europe for 2025 and beyond

)

The EU is transforming tax compliance with the VAT in the Digital Age (ViDA) Directive, adopted on November 5, 2024, and awaiting European Parliament approval. This directive aims to simplify and harmonize e-invoicing across the EU for a more efficient VAT system.

Here’s a quick guide to the key changes involved by ViDA and by the local regulations that are being implemented, focusing on France, Germany, Poland, Spain, and Belgium, Belgium, where mandatory e-invoicing rollouts begin in 2025-2026.

What is ViDA?

The ViDA Directive introduces mandatory e-invoicing and VAT data e-reporting across all EU member states over the next decade. It builds on three pillars, with the first focusing on e-invoicing reforms to modernize VAT reporting. Key highlights include:

Elimination of the buyer’s prior approval requirement, which was a major obstacle to the widespread adoption of e-invoicing.

Authorization of mandatory B2B e-invoicing, removing the need for EU exemptions and simplifying implementation across member states in the next five years.

Mandatory e-invoicing and VAT e-reporting for cross-border transactions, effective July 1, 2030.

EN16931 default standard for all domestic and cross-border B2B transactions from 2030.

Harmonization of e-invoicing and e-reporting systems, likely following a five-corner model (as in France), by 2035.

This directive will have significant implications across the European Union. Some countries, like Italy, will need to adapt existing reforms, while others will use ViDA as the foundation to launch their regulatory initiatives and prepare for 2030.

How is e-Invoicing implemented across key European markets?

Several EU countries have already started implementing e-invoicing ahead of ViDA. Five countries will introduce mandatory e-invoicing in 2025 or 2026. Here are the key details of these developments.

FRANCE

Timeline:

September 1, 2026: Mandatory invoice reception for all businesses and issuance for large companies (revenue > €50M and >250 employees).

September 1, 2027: Mandatory invoice issuance for all businesses.

System Set-up:

Scope: The e-invoicing obligation applies to all domestic B2B invoices.

The e-reporting obligation applies to all other VAT-related transactions (international B2B and B2C).

European standard EN16931 (XML UBL and CII) and Factur-X (PDF and XML CII).

Other formats can be used if both parties agree, and the required data can be extracted.

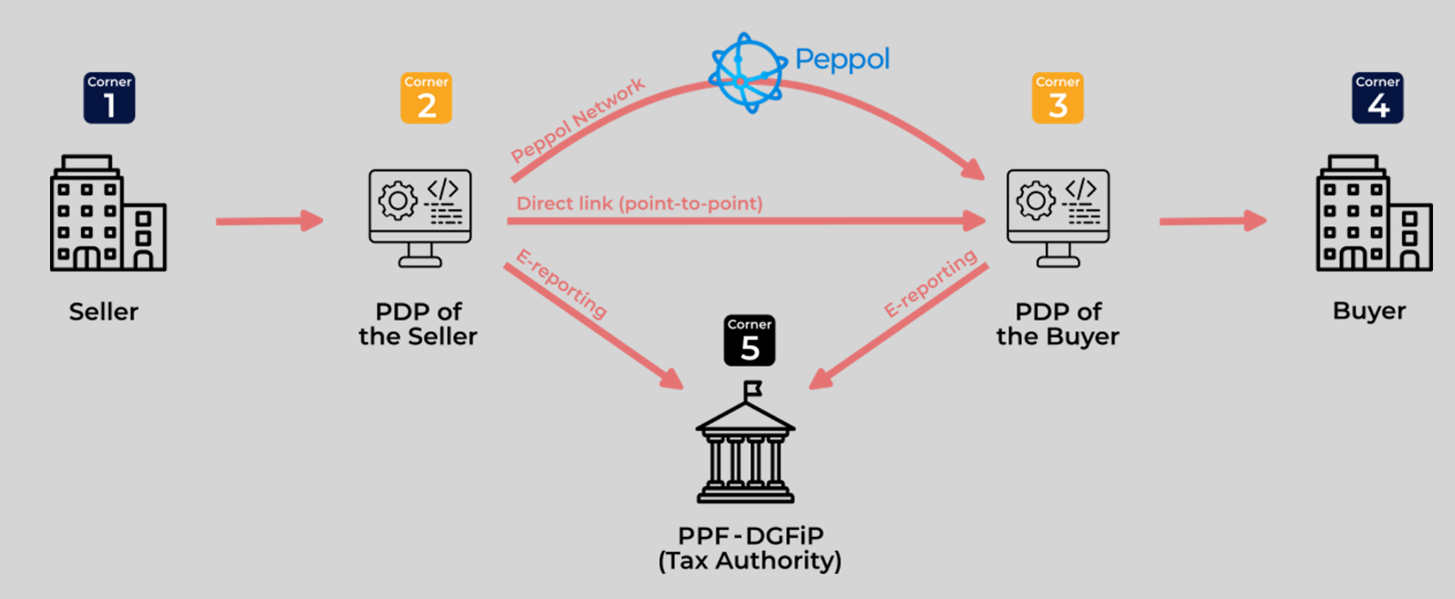

The system relies on private platforms (“PDPs” = Plateformes de Dématérialisation Partenaires) registered with the French tax authorities.

PDPs transmit data in real-time for domestic B2B transactions or periodically for international B2B and B2C transactions to the State’s central platform called “PPF” (Portail Public de Facturation).

Decentralized 5-Corner Model in France

Source: The Invoicing Hub

GERMANY

E-invoicing has been mandatory for B2G transactions since November 2020 (for the federal government and five regions; for others, only the obligation to receive electronic invoices is enforced). The new e-invoicing reform extends the obligation to B2B transactions, with e-reporting expected to be included soon.

Timeline:

January 1, 2025: Mandatory invoice reception for all businesses.

January 1, 2027: Mandatory invoice issuance for SMEs and large companies (revenue > €800K).

January 1, 2028: Mandatory invoice issuance for all businesses.

System Set-up

Scope: The new obligation applies to domestic B2B invoices, excluding low-value invoices (< €250) and travel expenses.

Formats: Compliance with the European semantic standard EN16931 (XML UBL and CII).

Formats like ZUGFeRD, X-Rechnung, Peppol BIS 3.0 are also accepted.

Other formats are allowed if both parties agree, and the required standard data can be extracted.

POLAND

For B2G transactions, only the obligation to receive invoices has been implemented so far.

The new e-invoicing reform introduces mandatory e-invoicing for all B2B and B2G transactions.

Timeline:

February 1, 2026: Obligation for companies with revenue exceeding 200 million PLN.

April 1, 2026: Obligation for all other companies.

System set-up:

Scope: Mandatory for all domestic B2B and B2G invoices (optional for B2C transactions).

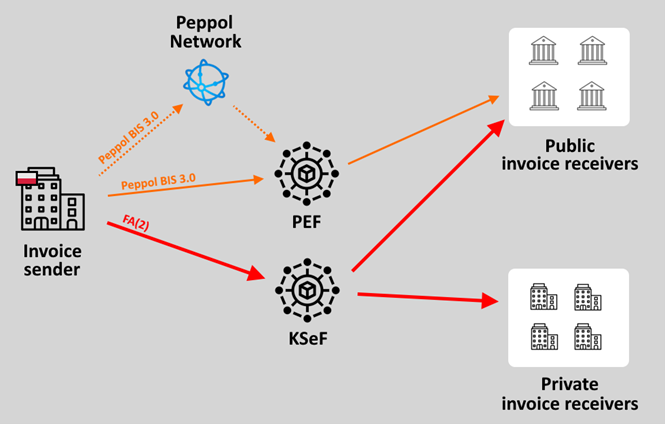

Formats: XML “FA(3)” specific to Poland.

Exchange Model: Centralized pre-Clearance model A centralized pre-clearance model (similar to the Italian system), requiring a “UPO” receipt for each submitted invoice, is implemented through a central platform called “KSeF” (Krajowy System e-Faktur).

For B2G transactions, the “PEF” (Platformy Elektronicznego Fakturowania) platform, connected to the Peppol network, can also be used.

E-reporting to the tax authorities is automated via e-invoicing.

Centralized pre-Clearance model in Poland

BELGIUM

E-invoicing for B2G has been mandatory in Belgium since 2020, facilitated through the Mercurius portal and the Peppol network.

The new e-invoicing reform extends this obligation to B2B transactions.

Timeline: January 1, 2026: Mandatory B2B e-invoicing for all companies.

System set-up:

Scope: The obligation applies exclusively to B2B invoices.

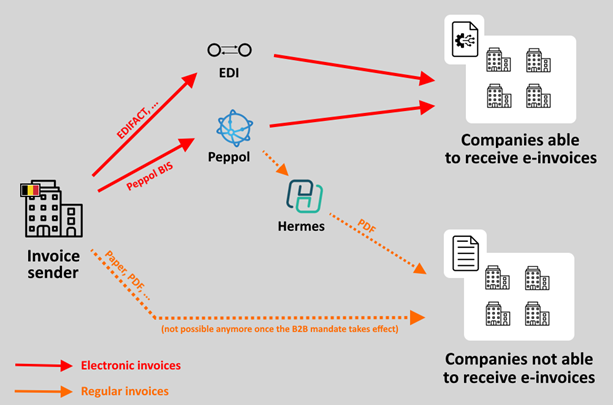

Formats: Peppol BIS 3.0 Invoice (compliant with the EN16931 standard) via the Peppol network, or other formats through alternative channels if both parties agree.

Exchange Model – Decentralized B2B network: Companies are encouraged to choose operators connected to the Peppol network but may also exchange directly.

Initially, a public platform called “Hermes”, linked to the Peppol network, will be available for free by default to invoice receivers. The latter will receive a PDF and the XML file of the invoice via email.

Alternatively, receivers can migrate to a private platform of their choice capable of handling electronic invoices.

Decentralized B2B network in Belgium

Source: The Invoicing Hub

SPAIN

Spain introduced mandatory B2G e-invoicing in 2015 via the “FACe” platform, with most regions adopting it, except for the Basque Country, which follows its own timeline. Mandatory e-reporting (SII) has been required since 2017 for companies with revenues over €6 million.

A new B2B e-invoicing mandate was planned for small businesses by July 2025 but is likely delayed. A new decree will clarify the timeline for this reform.

Timeline: Originally scheduled for January 1, 2024, and January 1, 2025, the obligation has been postponed indefinitely (likely no earlier than 2026–2027).

System Set-up:

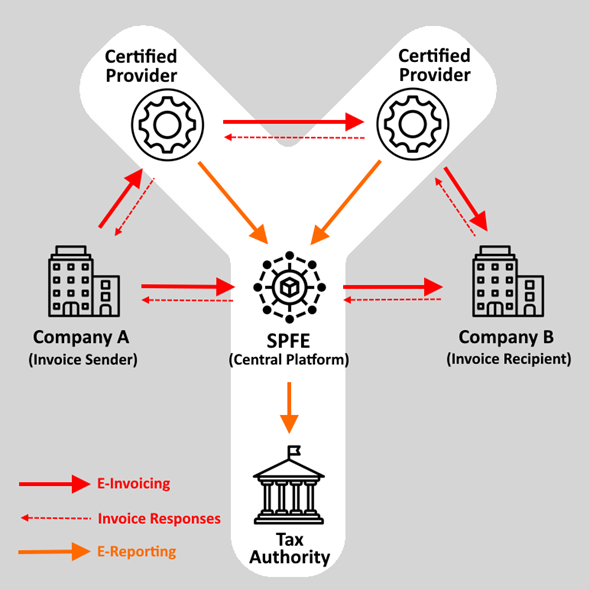

Scope: The new e-invoicing mandate applies to B2B invoices and includes e-reporting to the central tax administration.

Formats: FacturaE (XML) format via the public platform, or other formats (e.g., XML UBL, EDIFACT, or XML CII compliant with the European EN16931 standard) for exchanges between private platforms.

Exchange Model – Decentralized 5-Corner: Similar to the initial French model, Spain’s system will feature a central platform, “SPFE” (Solución Pública de Facturación Electrónica), and certified private platforms that report the required data to the Tax Administration.

Decentralized 5-Corner Model in Spain

Source: The Invoicing Hub

How can you prepare?

Understand the timeline: Identify when new e-invoicing rules apply in the countries where you operate.

Adopt the standards: Familiarize yourself with the EN16931 standard and other accepted formats.

Partner with experts: Work with a trusted provider to ensure compliance and streamline your e-invoicing processes.

Stay Ahead with TecAlliance

ViDA represents a massive shift in how businesses handle VAT reporting. Whether you’re already operating in a country with e-invoicing mandates or preparing for upcoming changes, early adoption is key to staying compliant.

Need Help? Learn how we can simplify e-invoicing for your business. Contact our experts.